The Power of Tax-Efficient Compounding

Published on December 7, 2021

With day trading making headlines, it seems that many investors have lost focus on the value of a buy-and-hold approach. We explain why it may make sense to harness the potential power of tax-efficient compounding when it comes to long-term wealth creation.

When it comes to saving and investing for the long term, the legendary investor Warren Buffett often comes to mind. But it’s also worth noting the contributions of Charlie Munger, Buffett’s long-time partner. Munger, a lawyer by training whose broad set of interests led him to investing later in life, has commented that “the elementary mathematics of compound interest is one of the most important models there is on earth.” He has also said: “the first rule of compounding: Never interrupt it unnecessarily.” Critical to this piece of advice are taxes and the long-term implications they can have on wealth accumulation.

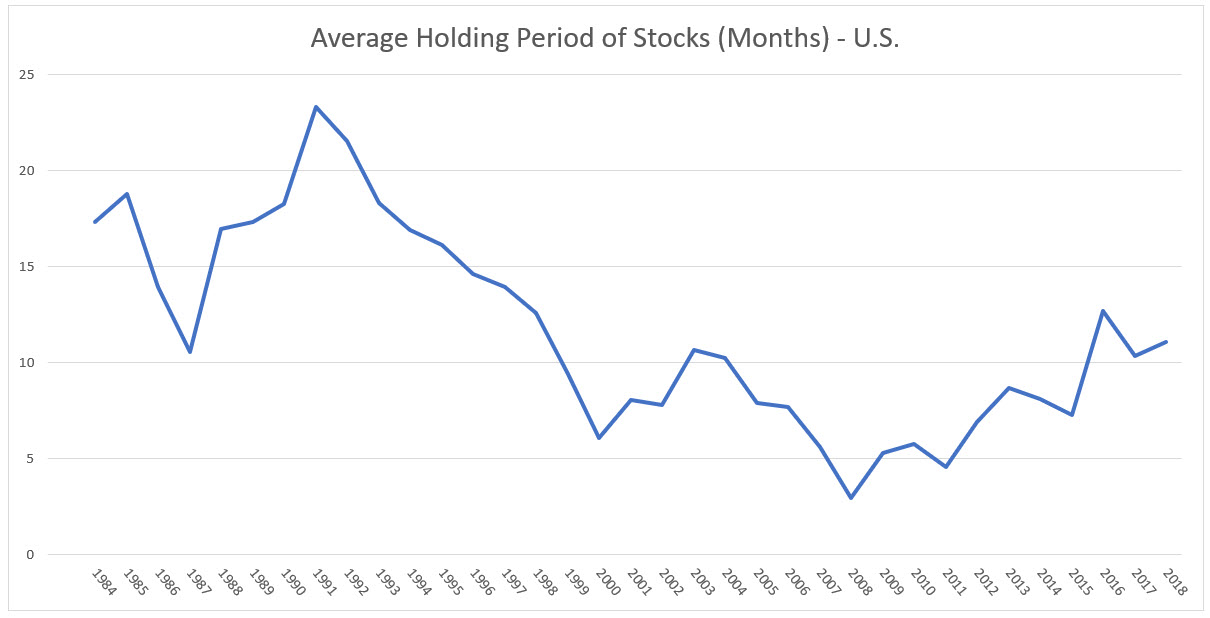

A key advantage of public equity investing is the ability to hold an investment for years. This allows investments to compound in a tax-efficient manner over long periods of time. Unfortunately, the typical investor does not capitalize on this opportunity. In fact, the average holding period for public equities in the U.S. has declined for decades:

More recent data suggests an average holding period of just 5.5 months as of June 20201. This holding period translates to over 200% annualized turnover for the average stock!

Compounding returns for years and even decades without having to pay taxes on interim gains (apart from taxes on dividend income) creates a massive structural advantage, versus earning similar returns in a more typical high-turnover strategy.

To understand what this can mean in practical terms, let’s explore two simple hypotheticals.

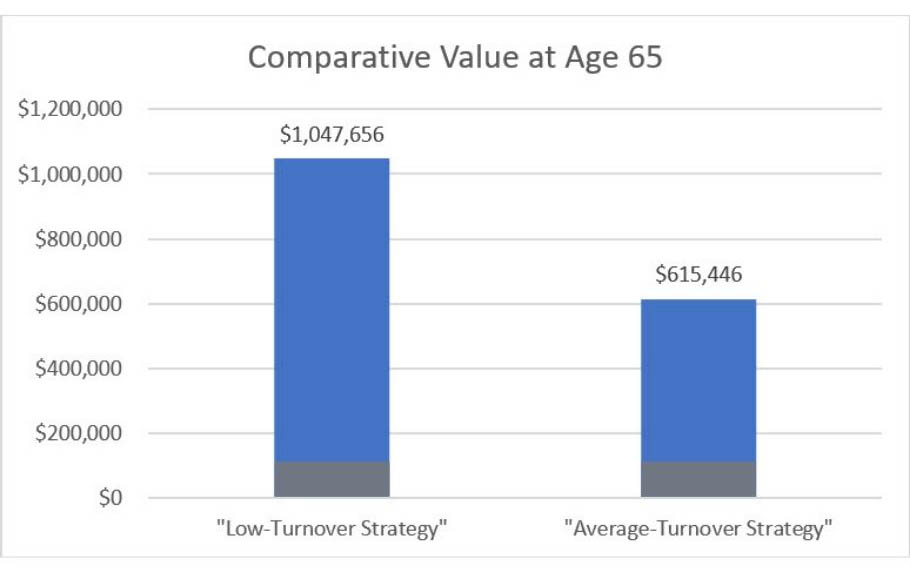

Let's say you invest $100,000 at age 35 in shares that pay no dividend and grow at 10% annually, what could be considered a respectable, but achievable, return based on long-term historical returns for equities. Assuming a holding period of three years, roughly in line with the average holding period for our Core Equity strategy, this investment would grow to over $1 million by age 65. Note that because of the longer holding period, gains are taxed at the current long-term capital gains rate of 20%. Let's call this the "low-turnover strategy."

If you instead invested that same $100,000 at age 35 in shares that grew at 10% annually but sold twice a year (roughly in line with the average holding period for the stock market), paid short-term capital gains taxes at a rate of 37%, and reinvested the after-tax amount into a new investment that generated that same exact 10% return, you'd have over $600,000 by age 65. Let's call this the "average-turnover strategy."

Even setting aside taxes, it is worth noting that executing a typical short-term strategy is very treacherous. Finding a sound investment generating 10% annual returns, then selling it at just the right time and immediately reinvesting all proceeds into the next investment that also meets your quality and return hurdles opens you up to a plethora of possible mistakes. Doing this well for years is exceedingly difficult. In our view, the more decisions you make, the more potential mistakes you encounter.

Even assuming perfect execution with zero mistakes, the "low-turnover strategy" clearly stands head and shoulders above the "average-turnover strategy" and results in well over $400,000 of added wealth, a 70% advantage.

Source: Osterweis Capital Management

The Core Equity team at Osterweis Capital Management takes long-term investing and tax management seriously. In fact, we've held some positions for over ten years and think carefully about tax implications when exiting or trimming positions.

This is not to say tax considerations should ever be the main factor in an investment: We center every conversation around business quality, competitive advantage, and the prospective return of an investment. But intelligently incorporating tax considerations into a long-term investment strategy could have a very beneficial impact on wealth creation over time.

Nael Fakhry

Co-Chief Investment Officer – Core Equity

Opinions expressed are those of the author, are subject to change at any time, are not guaranteed and should not be considered investment advice.

Osterweis Capital Management does not provide tax, legal or accounting advice. In considering this communication, you should discuss your individual circumstances with a professional in those areas before making any decisions.